CAPITAL ADJUSTERS REPORTS

Information on Repossession and Remarketing Issues

May 2016

Russ DeWitt, Editor

President, Capital Adjusters, Inc.

Past President, Nat'l Finance Adjusters

Member:

American Recovery Association

Recovery Specialist Insurance Group

Calif. Assn of Licensed Repossessors

Certified Asset Recovery Specialist

Certified Recovery Agent

____________________________

____________________________

CFPB Monitoring You and Your Repossession Vendor (Part 1)

CFPB Monitoring You and Your Repossession Vendor (Part 1)

____________________________

REPOSSESSIONS & REMARKETING

Newsletter

Who is the CFPB?

The Consumer Finance Protection Bureau (CFPB) was created and authorized by the Dodd-Frank Wall Street Reform Act that passed in 2010 in response to the financial crises of 2008. The announcement on that date put financial institutions and their service providers on notice with its publication titled CFPB to Hold Financial Institutions and their Service Providers Accountable. The publication went on to say that banks and nonbanks must responsibly manage their service provider relationships. That was 4 years ago.

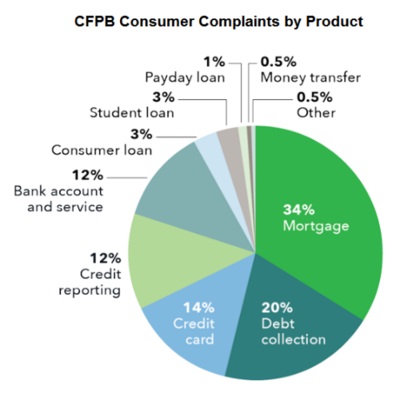

Fast forward to May of 2016 and we see just how much the CFPB has evolved and the impact that is already being felt on the industry. We have all heard or read of the substantial fines that have been handed down for failure to comply with these federal regulations. Most in the industry are also familiar with the CFPB’s Consumer Complaint database enabling consumers to file online complaints regarding consumer financial products. In many cases the monetary damage is outweighed by the reputational damage that a financial institution incurs. There are currently in excess of 541,000 complaints that have been filed and forwarded to over 3000 companies for responses.

To get a better idea of the impact that the CFPB has had in it’s fairly short existence here are the numbers reported by the CFPB on July 15th, 2015.

$10.1 Billion: Approx. amount of relief to consumers from CFPB enforcement activity.

17 Million: Consumers who will receive relief from CFPB enforcement activity.

$286 Million: Money ordered paid in civil penalties from CFPB enforcement activity.

$248 Million: Monetary relief provided to consumers from CFPB supervisory actions.

1.8 Million: Consumers who have received relief from CFPB supervisory actions.

One may question what all of this signifies to the asset recovery industry. The answer is quite simple. If a repossession agency contracts with your financial institution, then that agency must also comply with the federal guidelines set forth by the regulators. Title X of the Dodd-Frank Act authorizes the CFPB to (a) obtain and examine reports from supervised banks and non-banks for compliance with federal consumer financial law “and for other related purposes,” and to exercise enforcement authority when violations are identified; and (b) to exercise supervisory and enforcement authority over supervised service providers, including the authority to examine their operations on-site.

We must agree that the practice of repossessing collateral carries a higher risk than just about any other service contracted by a financial institution. The face to face interaction with the consumer during and post repossession increases the need to mitigate risk. These institutions are expected to adopt risk management processes commensurate with the level of risk and complexity of its third-party relationships. Over the past 4 years, financial institutions have started implementing their compliance monitoring systems which is evident from the increase in lender site visits and the increased requests for compliance related items. Routine sales calls have gone from one of a repossession service provider selling his/her knowledge of repossessing collateral to now having to demonstrate his/her knowledge of compliance and demonstrating that they have a compliance monitoring system in place for their agency. As was made clear over 3 years ago, during an industry webinar sponsored by VTS and presented by Attorney Michael Dougherty of Weltman, Weinberg & Reis, Mr. Dougherty said, “Folks, you now operate in a federally regulated industry. It may take a few years before we see a direct impact on the auto finance and repossession industry but it will be impacted.”He was spot on with his prediction.

(In Part 2: What does CFPB compliance of third party vendors mean for financial institutions?)

Part 1 of this series is reprinted from an article written by Max Pineiro of Vendor Transparency Solutions (VTS).

On April 13th 2012 the asset recovery industry started to undergo the largest transformation in its history, from a predominantly unregulated industry to one that is now federally regulated.